What Is Macroeconomics?

Macroeconomics is the study of the economy as a whole.

Instead of looking at one household, one business or one market, macroeconomics looks at the bigger picture. It examines national income, economic growth, inflation, unemployment, interest rates, government spending, taxation, trade and the overall financial conditions that affect people and businesses.

When news reports discuss whether the UK economy is growing, whether inflation is falling, whether interest rates may change or whether unemployment is rising, they are usually talking about macroeconomic issues.

Macroeconomics can sound technical, but the ideas behind it affect everyday life. It helps explain why prices rise, why jobs can become harder to find, why mortgage payments change, why governments borrow money and why economic growth matters.

Understanding macroeconomics can make financial news easier to follow and help readers see how national economic decisions can filter down into household and business finances.

Macroeconomics In Simple Terms

In simple terms, macroeconomics is about the whole economy.

It asks questions such as:

- Is the economy growing or shrinking?

- Are prices rising too quickly?

- Are people able to find work?

- Are wages keeping up with inflation?

- Is the government spending more than it receives in tax?

- Are interest rates encouraging or slowing borrowing?

- Is the country importing more than it exports?

These questions are much broader than the decisions made by one person or company. Macroeconomics looks at patterns across millions of households, businesses, workers, consumers and public bodies.

For example, one person losing a job is a personal financial issue. A rise in unemployment across the country is a macroeconomic issue.

One shop increasing prices is a business decision. Prices rising across the economy is inflation, which is a macroeconomic issue.

Macroeconomics And Microeconomics

Macroeconomics is often compared with microeconomics.

Microeconomics looks at smaller units within the economy. It studies the choices made by individuals, households, businesses and specific markets. For example, microeconomics might look at why a customer chooses one product over another, how a business sets prices or how supply and demand affect the housing market.

Macroeconomics looks at the overall economy. It studies national output, employment, inflation, interest rates, public finances and economic growth.

The two areas are connected. Individual choices affect the wider economy, and the wider economy affects individual choices.

For example, if many households reduce spending because prices are rising, businesses may see lower demand. If businesses then cut hiring, unemployment may rise. That becomes a macroeconomic issue.

GDP And Economic Growth

Gross domestic product, or GDP, is one of the most important concepts in macroeconomics.

GDP measures the value of goods and services produced in an economy over a period of time. It is commonly used to judge whether an economy is growing or shrinking.

If GDP rises, the economy is usually producing more than before. If GDP falls, the economy is producing less.

Economic growth matters because it can affect employment, wages, government tax receipts, business confidence and public spending. A growing economy may create more opportunities for workers and firms, while a shrinking economy may lead to caution, job losses or reduced investment.

However, GDP is not a perfect measure of wellbeing. It does not show how income is shared or whether households feel financially secure.

For a fuller explanation, our guide to UK GDP explained looks at what GDP means and why it matters for households and businesses.

Inflation

Inflation is another central macroeconomic topic.

Inflation means prices are rising across the economy. If inflation is high, the cost of goods and services increases more quickly. This can reduce the value of money because the same income buys less than before.

For households, inflation can affect food bills, energy bills, rent, transport, insurance and other everyday costs. For businesses, inflation can increase wages, materials, energy costs and operating expenses.

Inflation can also affect interest rates. Central banks often raise interest rates when inflation is too high, because higher rates can reduce borrowing and spending. This may help slow price rises, but it can also make mortgages, loans and business finance more expensive.

A moderate level of inflation is often seen as normal in a modern economy. The problem comes when inflation rises too quickly, stays high for too long or becomes difficult for households and firms to manage.

Unemployment

Unemployment measures the number of people who are looking for work but do not currently have a job.

It is an important macroeconomic indicator because work is one of the main ways people earn income. When unemployment is low, more people are in work, tax receipts may be stronger and household spending may be more stable.

When unemployment rises, more people may need support, household incomes can fall and consumer confidence may weaken. Businesses may also become more cautious if demand is falling.

Unemployment can rise during recessions, but it can also be affected by changes in technology, industry, skills, regional conditions and business confidence.

A low unemployment rate does not always mean everyone is financially comfortable. Some people may be in insecure work, low-paid work or jobs with limited hours. This is why economists also look at wages, underemployment and job quality.

Interest Rates

Interest rates are a major part of macroeconomics because they influence borrowing, saving and spending.

When interest rates rise, borrowing usually becomes more expensive. This can affect mortgages, credit cards, personal loans, business loans and government borrowing. Higher rates may encourage saving, but they can also put pressure on households and firms with debt.

When interest rates fall, borrowing may become cheaper. This can support spending and investment, but it may also reduce returns for savers.

In the UK, the Bank of England sets Bank Rate, which influences interest rates across the wider economy. It does this mainly to help control inflation.

Interest rates show how macroeconomics can affect everyday financial decisions. A national rate decision can change monthly mortgage costs, savings returns and business finance conditions.

Government Spending And Taxation

Government spending and taxation are important macroeconomic tools.

Governments spend money on public services, benefits, pensions, infrastructure, defence, education, healthcare and other areas. They raise money through taxes such as income tax, National Insurance, VAT, corporation tax, council tax and fuel duty.

When government spending is higher than tax revenue, the government usually borrows. This creates a budget deficit. Over time, borrowing adds to public debt.

Public finances are closely linked to economic growth. When the economy grows, tax receipts often rise. When the economy weakens, tax receipts may fall and demand for support may increase.

Government spending can also influence the economy directly. For example, infrastructure investment may support jobs and business activity, while benefit payments can support household incomes.

Recession

A recession is commonly described as two consecutive quarters of falling GDP.

A quarter is a three-month period. If the economy shrinks for two quarters in a row, it is usually described as being in recession.

Recessions can happen for many reasons. These may include financial crises, high inflation, rising interest rates, falling consumer spending, external shocks, business uncertainty or global events.

During a recession, businesses may reduce investment, unemployment may rise and households may become more cautious. Government finances can also come under pressure because tax receipts may fall while demand for support increases.

Not all recessions are the same. Some are short and mild, while others are deep and long-lasting.

Looking at the UK economic growth rate through history can help show how recessions and recoveries have shaped the economy over time.

Trade And The Global Economy

Macroeconomics also looks at trade between countries.

The UK imports goods and services from abroad and exports goods and services to other countries. Trade affects prices, jobs, business activity, exchange rates and economic growth.

If imports become more expensive, this can push up prices for consumers and businesses. If exports grow, businesses may benefit from stronger demand overseas.

Exchange rates also matter. A weaker pound can make imports more expensive but may make UK exports more competitive. A stronger pound can make imports cheaper but may make exports less competitive.

Because the UK is part of a global economy, domestic growth is affected by international events. Energy prices, wars, supply chains, financial markets and global demand can all influence UK macroeconomic conditions.

Productivity

Productivity measures how much output is produced for each worker or each hour worked.

It is one of the most important long-term drivers of living standards. If workers and businesses can produce more value in the same amount of time, wages and profits may be able to rise without creating the same inflationary pressure.

Productivity can improve through better technology, training, infrastructure, management, investment and innovation.

Weak productivity growth has been a major concern for the UK economy in recent years. If productivity grows slowly, the economy may struggle to achieve strong wage growth and rising living standards.

This is why productivity appears often in economic debates, even if it sounds less familiar than inflation or interest rates.

Why Macroeconomics Matters To Households

Macroeconomics matters because national economic conditions affect household finances.

Inflation affects the cost of living. Interest rates affect mortgages, rent pressures, savings and borrowing. Unemployment affects job security. Economic growth affects wages, business confidence and public finances.

Government tax and spending decisions can influence benefits, public services, pensions, childcare, transport and local support.

Households do not experience the economy in exactly the same way. A homeowner with a mortgage may feel interest rate changes differently from a renter. A pensioner may be affected differently from a student. A business owner may be affected differently from an employee.

Even so, macroeconomic trends shape the background conditions behind many personal financial decisions.

Why Macroeconomics Matters To Businesses

Businesses are affected by the wider economy every day.

When the economy is growing, customers may spend more, firms may invest and lenders may be more confident. When the economy is weak, businesses may face lower demand, higher caution and tighter margins.

Inflation can increase costs. Interest rates can make borrowing more expensive. Exchange rates can affect imports and exports. Government policy can affect tax, regulation, grants and public contracts.

Small businesses can be especially sensitive to macroeconomic conditions because they may have less cash available to absorb shocks.

Understanding macroeconomics can help business owners read the wider environment more clearly, even though it cannot predict every challenge.

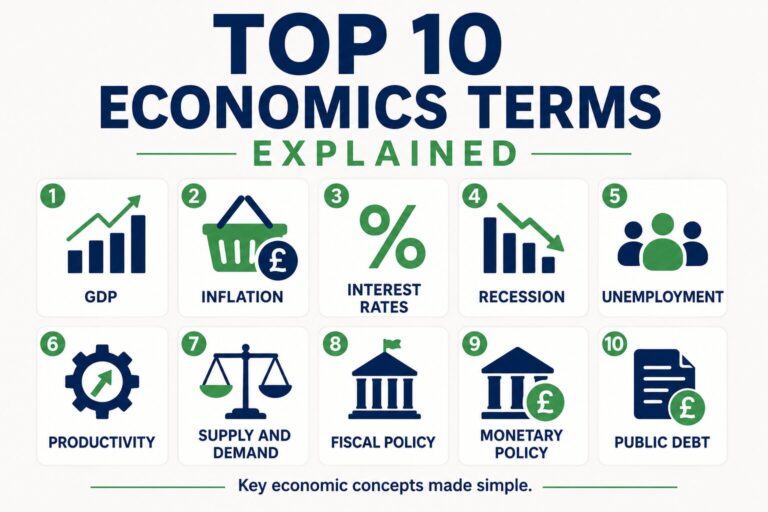

Common Macroeconomic Terms

Macroeconomics includes many terms that appear regularly in the news.

These include GDP, inflation, deflation, recession, productivity, unemployment, interest rates, fiscal policy, monetary policy, public debt, trade deficit and exchange rates.

Some terms are easy to confuse. For example, inflation means prices are rising, while deflation means prices are falling. A deficit usually refers to annual borrowing, while debt refers to the total amount owed.

For readers who want a clearer glossary, our guide to macroeconomic terms defined explains many of these concepts in more detail.

Clear Economic Writing

Economic language can make important topics feel more complicated than they need to be. Clear explanations are useful because they help readers understand the link between national figures and everyday financial pressure.

Commerce Grants publishes plain-English guides on economics, finance, grants, education funding and government support. Writers who want to explain economic topics in plain English can review our Write For Us Finance page.

Strong economic writing should explain what a term means, why it matters and how it may affect readers without making unrealistic predictions.

Conclusion

Macroeconomics is the study of the economy as a whole. It looks at GDP, inflation, unemployment, interest rates, government spending, taxation, trade, productivity and economic growth.

These topics may sound abstract, but they affect everyday life. They influence prices, wages, jobs, mortgages, savings, business confidence, public services and government support.

Macroeconomics does not explain every individual financial situation, but it helps describe the wider conditions that shape households, businesses and public finances.

Understanding macroeconomics makes it easier to follow economic news, compare policy decisions and see why changes in growth, inflation or interest rates can matter beyond the headlines.